{kind=link}

Annaly Capital (NLY 0.66%) has an enormous dividend yield that approaches 15%. And the mortgage actual property funding belief (REIT) simply elevated its dividend at the beginning of 2025. However do not get lured in by the yield if you’re searching for a dependable dividend inventory.

You may be higher off with decrease yields from rising companies like Agree Realty (ADC -0.39%) and PepsiCo (PEP -1.51%). This is why these two dividend payers are prone to be value greater than Annaly in 5 years.

The massive drawback with Annaly Capital

Annaly Capital really achieves what it units out to do, so it is not a foul mortgage REIT. The issue is the mortgage REIT mannequin, which entails shopping for mortgages which have been pooled into bond-like securities. The purpose is to pay out as excessive a dividend as attainable, however the expectation is that these dividends will get reinvested. The top result’s a powerful whole return.

If you happen to do not reinvest these dividends, nevertheless, the end result right here will doubtless be removed from fascinating — much less capital and fewer revenue, which is about as dangerous because it will get for a dividend investor. Primarily, a lot money goes out the door as dividends that the worth of the REIT’s portfolio shrinks over time.

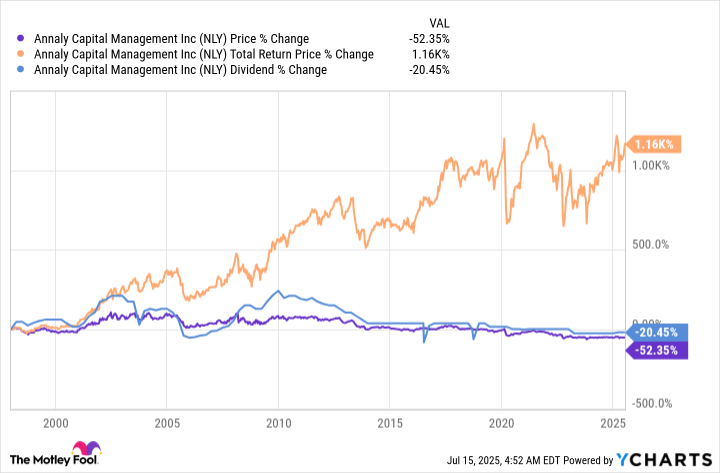

Sure, you will get an enormous yield within the close to time period. However buyers are principally getting their principal returned to them in that fats dividend. With much less cash to place to work for buyers, Annaly merely cannot keep the large dividend over the long run. There will probably be ups and downs primarily based on how mortgage bonds are performing over the brief time period, however the big-picture development is the one which long-term buyers want to look at.

Picture supply: Getty Photographs.

Rising companies are higher choices

A greater guess for many dividend buyers will probably be discovering lower-yielding shares with rising companies. For instance, fellow REIT Agree Realty has a yield of 4.2%. It buys single-tenant internet lease retail properties within the U.S., with tenants selecting up most property working prices. Roughly 5 years in the past it owned about 1,200 properties. On the finish of the primary quarter of 2025 it owned greater than 2,400 properties. Successfully, the scale of the corporate’s enterprise doubled.

Whereas the expansion is definitely pretty spectacular, it is not actually stunning. Your entire function of the REIT is to extend the scale of its portfolio over time by shopping for extra properties. That permits it to pay a lovely dividend that additionally grows over time. Through the previous 5 years Agree’s dividend has risen at about 5% a yr, on an annualized foundation. Because the enterprise and dividend develop over the long run, buyers are inclined to reward firms like Agree with the next inventory worth.

An alternative choice is to purchase an organization like PepsiCo, which has seen its inventory worth tumble roughly 30% from the highs it reached in 2023. That drop has pushed the dividend yield as much as a traditionally excessive 4.3% or so. As soon as once more, nevertheless, the enterprise backing the dividend is concentrated on development.

For instance, regardless of the comparatively weak working outcomes PepsiCo is placing up immediately, it just lately purchased two smaller rivals. Poppi added probiotic drinks to the portfolio and Siete added Mexican American meals; each will assist PepsiCo sustain with altering shopper tastes. And they’re going to assist the Dividend King proceed to increase its spectacular streak of annual dividend will increase, which now stands at 53 years. The dividend has grown at a roughly 7% annualized tempo throughout the previous 5 years.

The issue is not Annaly

As famous, Annaly is not a foul firm. It’s only a very distinctive funding due to the character of its enterprise. Over time the worth of the mortgage portfolio it owns, which is basically the worth of the corporate, is shrinking. That huge yield is not what it appears and is not prone to be sustainable, and certainly it has been reduce because the inventory worth declines. Not less than that is what historical past suggests right here.

Most dividend buyers will probably be higher off shopping for decrease, although nonetheless engaging, yields on provide from rising firms like Agree and PepsiCo.