{kind=link}

Meta pays Alphabet $10 billion over six years for entry to Google Cloud’s infrastructure.

The shares of Google father or mother Alphabet (GOOGL 3.10%) (GOOG 2.98%) and Meta Platforms (META 2.04%) shot greater in Friday buying and selling. Though most shares rose as a result of the Federal Reserve strongly hinted at a September reduce in rates of interest, one other issue was possible the announcement of Meta’s cloud cope with Google, as reported by The Data.

Contemplating the $10 billion dimension of the deal, one has to imagine it’s crucial, notably to Alphabet. Nonetheless, contemplating the state of the synthetic intelligence (AI) inventory, it may function a much-needed catalyst for the corporate’s traders. This is why.

Picture supply: Getty Photos.

Phrases of the partnership

Underneath the phrases of the deal, Meta pays Google $10 billion over six years. In alternate, it is going to obtain entry to Google Cloud’s storage, server, and networking providers, together with different merchandise.

Meta has beforehand relied on Amazon‘s Amazon Internet Providers (AWS) and Microsoft‘s Azure for such providers. The deal doesn’t essentially imply it is going to deal much less with these firms. Extra possible, it speaks to Meta’s insatiable demand for cloud infrastructure because it seeks to turn into a significant participant within the AI house.

Moreover, Meta and Alphabet are one another’s largest opponents within the digital promoting market. And within the first half of 2025, 98% of Meta’s income got here from digital adverts. Therefore, in a way, it’s outstanding that these two would turn into companions in a distinct enterprise.

The way it helps Alphabet

Nonetheless, in one other sense, it is a big step ahead for Alphabet’s future. Within the first half of this yr, Alphabet earned 74% of its income from the digital advert market, down from 76% in the identical interval in 2024. That is additionally by design, as Alphabet has bought dozens of companies unrelated to the digital advert market in its efforts to transition right into a extra diversified expertise enterprise.

To this point, Google Cloud is the one one in all these enterprises to look in Alphabet’s financials. It accounted for 14% of Alphabet’s income within the first two quarters of 2025, up from 12% in the identical year-ago interval.

Moreover, Google Cloud generated over $49 billion in income over the trailing 12 months, implying the $10 billion from Meta over six years will make up a comparatively small portion of Google Cloud’s enterprise.

Nonetheless, the deal serves as a vote of confidence for Alphabet’s cloud enterprise, one which continues to lag AWS and Azure by way of market share.

Picture supply: Statista. Y-o-y = yr over yr.

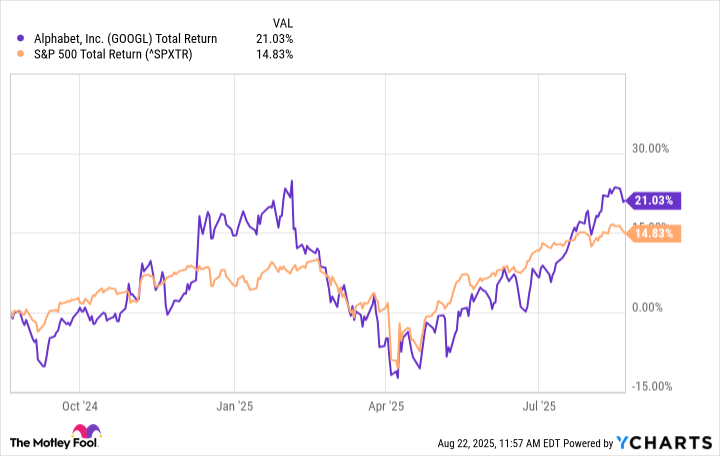

The investor perspective can also be essential. Over the past yr, Alphabet inventory has outpaced the entire returns of the S&P 500 by a major however not eye-popping margin. Nonetheless, it might assist that Alphabet’s price-to-earnings (P/E) ratio of twenty-two is the bottom amongst “Magnificent Seven” shares. Therefore, the Meta deal may immediate traders to look extra favorably upon that earnings a number of.

GOOGL Complete Return Stage information by YCharts.

Moreover, if the Meta deal prompts different firms to do extra enterprise with Google Cloud, it may present a lift to its market share and, by extension, Alphabet inventory.

The Meta deal and Alphabet inventory

Finally, Meta’s cope with Google Cloud will greater than possible take Alphabet inventory a leg greater, however traders ought to anticipate the results to be extra oblique. Certainly, the deal is outstanding in that it serves as a lift for third-place Google Cloud and is notable for the reason that two firms are direct opponents in one another’s largest enterprises.

Though $10 billion in added enterprise over six years is substantial, Google Cloud generated $49 billion over the past 12 months. Thus, it’s a important however not game-changing enhance to the enterprise.

Nonetheless, the deal might make Google Cloud extra enticing to potential prospects, and the low P/E ratio may entice extra traders to Alphabet. Ultimately, these may turn into the extra important advantages of the deal.

Will Healy has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and quick January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.