{kind=link}

The inventory’s endured a painful 55% slide over the previous few years. Nevertheless, issues may begin wanting up.

Goal (TGT -4.86%), the favored retail chain well-known for its pink bullseye brand, has been a stomach-churning funding for a number of years. The inventory has been on a gentle slide since late 2021 and sits 55% off its former excessive at the moment. The S&P 500 index has risen over 20% since then, so Goal’s struggles soar off the web page at you.

Much more head-scratching is that Goal is a blue chip firm with a well-liked model and an extended monitor document of success, not some unprofitable, high-risk moonshot wager. It is a Dividend King with 58 consecutive annual dividend will increase! That does not occur accidentally.

So why is Goal inventory performing so poorly, and is there sufficient worth right here to justify shopping for the inventory in March?

Explaining Goal’s struggles

A inventory’s worth motion influences an organization’s narrative. Look at Goal’s slide over the previous few years, and also you would possibly assume the enterprise is doing terribly. The truth is that Goal’s enterprise fundamentals are fairly strong (extra on that quickly). So why has Goal’s inventory fallen off so arduous?

It boils right down to Goal being a extra cyclical retail firm than its rivals.

When folks buy groceries, their spending tends to fall into two classes: discretionary (desires) and staples (wants). You want issues like groceries and family merchandise (e.g., toothpaste and cleaning soap). It’s your decision issues like furnishings, electronics, and new garments, however most individuals do not want them to get by.

Goal sells groceries and family staples, however these classes represented solely about 40% of merchandise gross sales final yr. Walmart, for one, sells extra staples; grocery alone made up 60% of its U.S. retailer gross sales final yr. In different phrases, Walmart tends to carry up higher when shoppers reduce.

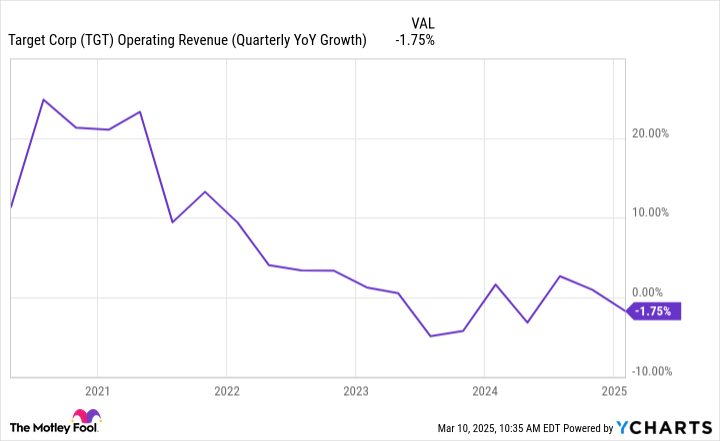

In 2020-2021, when the U.S. authorities despatched out stimulus checks to shoppers, discretionary spending within the financial system was boosted as a result of not everybody who received the stimulus wanted it. Then, as that cash dried up and inflation tightened budgets for a lot of People, discretionary spending dropped. You may see beneath how Goal’s income development fell off a cliff following the pandemic:

TGT Working Income (Quarterly YoY Progress) information by YCharts

The underside line? Goal’s enterprise is in a stoop and should stay so till discretionary spending recovers.

The corporate nonetheless sits on a robust monetary basis

However there is a distinction between a slumping firm and a damaged enterprise. It would not appear that Goal is in terminal decline, and it goes past the corporate’s decades-long monitor document.

The enterprise is financially strong in a number of methods. For instance, that well-known dividend yields 3.9% at the moment, approaching an all-time excessive. Abnormally excessive yields could be a pink flag, however Goal’s dividend payout ratio is just 45% of money move. Past that, the corporate is leveraged to only one.8 instances its earnings earlier than curiosity, taxes, depreciation, and amortization (EBITDA), has $4.7 billion in money, and enjoys an “A” credit standing. Goal’s dividend is in nice form regardless of the corporate’s lack of development.

Goal is working via a large stoop as a result of the COVID-19 stimulus created a colossal spending increase. There is a good likelihood that buyers will ultimately bounce again, and so ought to Goal. Till then, the inventory pays you to personal shares, and buyers should not lose a lot sleep over the corporate’s stability.

Ought to buyers purchase the inventory now?

To be honest, the inventory nonetheless is not some generational discount resulting from its decline.

Goal at present trades at a price-to-earnings ratio of slightly below 13. Analysts count on earnings to develop by a mean of simply over 6% yearly over the following three to 5 years. The ensuing PEG ratio (2.1) indicators that the inventory’s valuation is affordable for its anticipated development. In different phrases, one would possibly argue that Goal was overvalued popping out of the pandemic, and its decline, as painful because it was, has repriced the inventory extra appropriately.

May shares go decrease? In fact! Bear in mind, the inventory could wrestle till discretionary spending picks up once more. That stated, the inventory may ship strong whole returns (dividends and earnings development) between 10% and 11% yearly over time.

If that appeals to your investing objectives, Goal is a strong shopping for thought to contemplate this month.

Justin Pope has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Goal and Walmart. The Motley Idiot has a disclosure coverage.