Stock That Will Be Worth")

{kind=link}

Amazon’s progress charges are far superior to Apple’s.

Apple is the world’s third-largest firm by a large margin, with a $1 trillion hole between it and fourth-place Alphabet . Nonetheless, I feel a number of firms are slated to cross Apple in market share over the following 5 years, together with fifth-place Amazon (AMZN -0.00%), which is valued at round $2.4 trillion in comparison with Apple’s $3.5 trillion.

That is a large hole to make up in 5 years, however taking a look at Amazon’s progress tailwinds versus Apple’s makes it pretty clear that Amazon is the significantly better inventory choose.

Picture supply: Getty Pictures.

Amazon has two enterprise models driving revenue progress

Apple’s enterprise is pretty easy; it is the main client tech model and generates vital income promoting iPhones and different merchandise within the Apple ecosystem. Amazon is a little more advanced, because it has the web retailer that almost all buyers are conversant in, however that is not the very best cause to spend money on it.

Though its on-line shops division posted the very best quarter in a very long time (income rose 11% yr over yr), the actual stars of the present are Amazon Internet Providers (AWS) and its promoting companies division.

AWS is Amazon’s cloud computing platform, and it’s seeing sturdy demand fueled by the migration of conventional workloads to the cloud, in addition to by new synthetic intelligence (AI) workloads. AWS grew income by 17% yr over yr in Q2, which is powerful progress contemplating it generated practically $31 billion in income throughout the quarter. Nonetheless, AWS’s major rivals (Microsoft‘s Azure and Google Cloud) posted stronger progress charges of their corresponding quarters, so buyers are frightened about AWS’s long-term potential to carry out on this sector regardless of its being the market-share chief.

AWS will possible proceed to underperform its friends attributable to its dimension, however 17% progress is nothing to sneer at. AWS can also be a big a part of Amazon’s revenue image. In Q2, it accounted for 53% of Amazon’s working income regardless of accounting for under 18% of income. Analysts nonetheless anticipate cloud computing to develop quickly over the following few years, and if Amazon surpasses Apple in market cap, this shall be a major cause why.

Promoting companies is Amazon’s fastest-growing phase, with income rising 23% yr over yr, an acceleration over earlier quarters’ progress price. Amazon has probably the most profitable locations to promote on the web, as customers are already coming to their platform to make purchases. Paying to put a product on the high of an Amazon search virtually ensures elevated gross sales. That is price loads to its promoting shoppers and shall be a key a part of Amazon’s funding thesis over the following few years.

Amazon’s margins are rising

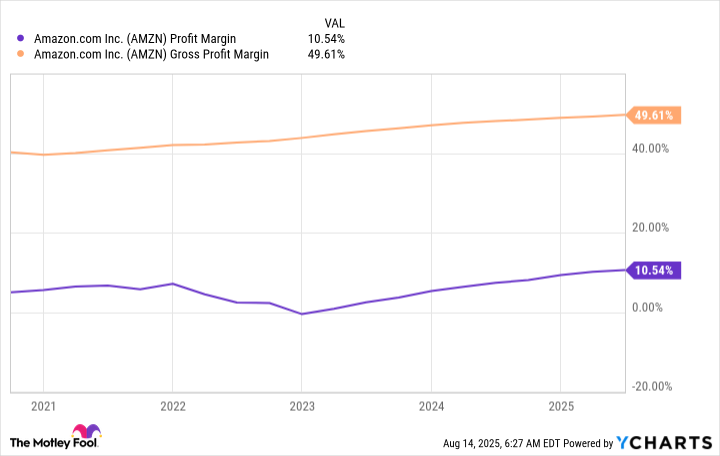

Amazon is not a income progress story; it is a revenue progress story. The rise of high-margin companies like AWS and promoting companies has helped Amazon increase its revenue margins over the previous few years.

AMZN Revenue Margin information by YCharts

With its two high-margin enterprise segments rising quicker than different components of its enterprise, Amazon will naturally have elevated revenue progress charges. In Q2, Amazon’s working earnings rose 31% yr over yr.

Distinction that with Apple, whose Q3 FY 2025 (ending June 28) working earnings elevated by 11%. Amazon’s revenue progress price is way quicker. Over 5 years, a 30% progress price will enhance its working earnings by 271% whereas an 11% progress price will increase working earnings by solely 69%.

That will be sufficient to drive Amazon’s income increased than Apple’s, propelling it to surpass it in dimension alongside the best way. Amazon is a wonderful inventory choose for the following 5 years and a no brainer purchase at right this moment’s costs.

Keithen Drury has positions in Alphabet and Amazon. The Motley Idiot has positions in and recommends Alphabet, Amazon, Apple, and Microsoft. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and quick January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.